GO-TO-MARKET STRATEGY - FOOD INDUSTRY

PLANT-BASED UK MARKET ENTRY

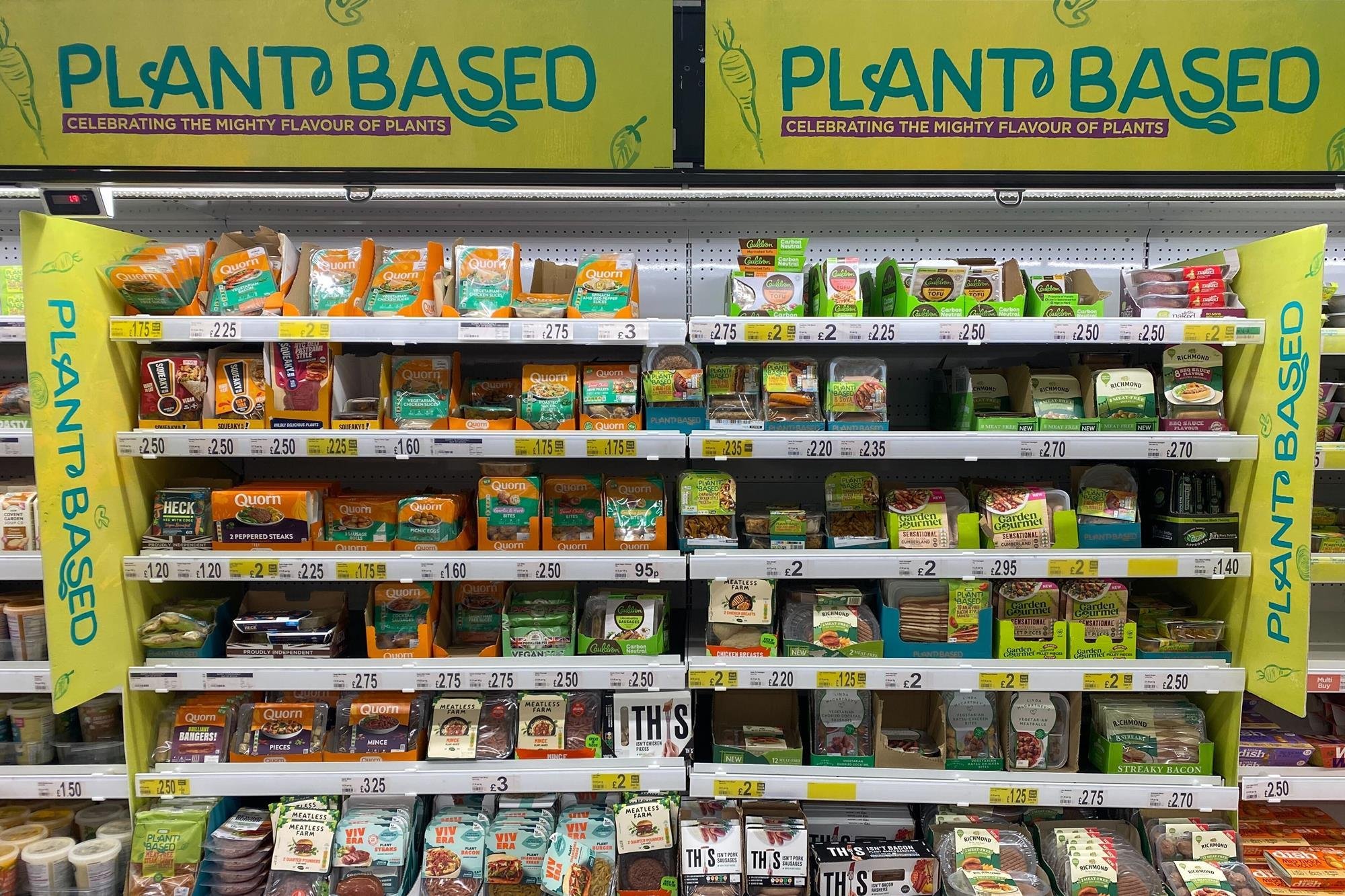

SITUATION

A leading European food company was exploring UK entry with a differentiatedclean-label vegetable slices proposition, built around natural ingredients rather than conventional meat-mimic alternatives.

The UK plant-based market represented an attractive but complex opportunity: retailers were still looking for credible growth platforms, while consumers were increasingly demanding healthier, less processed, and better-tasting options.

At the same time, the category was under pressure from UPF concerns, price sensitivity, retailer range rationalisation, and weak economics for several plant-based brands, making successful entry highly dependent on the right proposition, channel strategy, and execution model.

The client needed to understand whether its proposition could credibly unlock incremental category growth in the UK and how it should compete against established brands with stronger local awareness and retailer relationships.

PROJECT OBJECTIVE

Assess the attractiveness of the UK plant-based market and determine whether the client had a credible right to win, considering consumer needs, retailer priorities, competitive dynamics, and category profitability.

Define the optimal UK entry strategy across the key commercial levers: product, pack format, pricing, promotion, shelf placement, distribution scope, and launch sequencing.

Evaluate alternative go-to-market models, including direct branded entry, private label, partnership, and acquisition-led options, to identify the most viable route for scaling in the UK.

Quantify the expected commercial upside and contribution margin potential under different rollout scenarios, including the impact of pricing, promotional intensity, trade terms, logistics, A&P, and rate of sale.

WHAT WAS DONE

Analysed Nielsen sell-out data to quantify category size, growth, rate of sale, pricing, promotional intensity, regional performance, store-format dynamics, and the relative performance of leading brands and SKUs.

Conducted detailed retail store audits across key UK locations to assess pack-size norms, shelf placement, competitor facings, merchandising constraints, promotional mechanics, price architecture, and practical listing implications.

Ran bespoke consumer research to understand category barriers, usage occasions, purchase drivers, brand perceptions, and the relative appeal of a clean-label legume-based proposition versus existing plant-based meat alternatives.

Benchmarked leading UK plant-based players to identify sources of competitive advantage, brand weaknesses, whitespace opportunities, portfolio gaps, recent category exits, and potential acquisition or partnership platforms.

Conducted expert and retailer interviews to pressure-test hypotheses on listing requirements, retailer economics, shelf-life expectations, promotional models, merchandising standards, distribution priorities, and category growth drivers.

Developed a retail rollout analysis based on existing players, assessing store-format performance, regional growth potential, SKU productivity, launch benchmarks, promotional intensity, and rate-of-sale thresholds to inform distribution roll-out and execution risks.

RESULTS DELIVERED

Delivered a structured market-entry diagnostic covering market attractiveness, consumer demand, competitor positioning, retailer requirements, operational feasibility, and economic viability.

Identified the key adaptations required for UK success, including changes to pack format, slice size, price positioning, promotional strategy, shelf placement, and distribution focus.

Defined a recommended rollout strategy centred on hero SKUs, selective distribution in high-performing store formats, priority regional clusters, and disciplined expansion once rate-of-sale thresholds were proven.

Quantified the expected economics of entry and highlighted the most important profitability sensitivities, including rate of sale, promo depth, retailer margin, logistics costs, A&P investment, and distribution breadth.